Comparing car insurance rates can save money, but only when the comparison is fair. Many drivers look at the monthly premium first and assume the cheapest quote is automatically the best one. In reality, two quotes can look very different because the liability limits, deductibles, optional coverages, discounts, payment terms, and driver details are not the same.

This guide explains how to compare car insurance rates with more accuracy. The goal is not just to find the lowest number, but to understand whether a quote gives you the right balance of price, coverage, deductible comfort, claims protection, and provider fit.

Compare Equal Policies

Use the same liability limits, deductibles, vehicle details, driver information, and coverage choices for every quote.

Look Beyond Premium

The monthly payment matters, but deductible risk, fees, coverage exclusions, and claim support can change the real value.

Review Final Cost

Compare the final price after discounts, payment fees, and policy choices, not just the first number shown in a quote form.

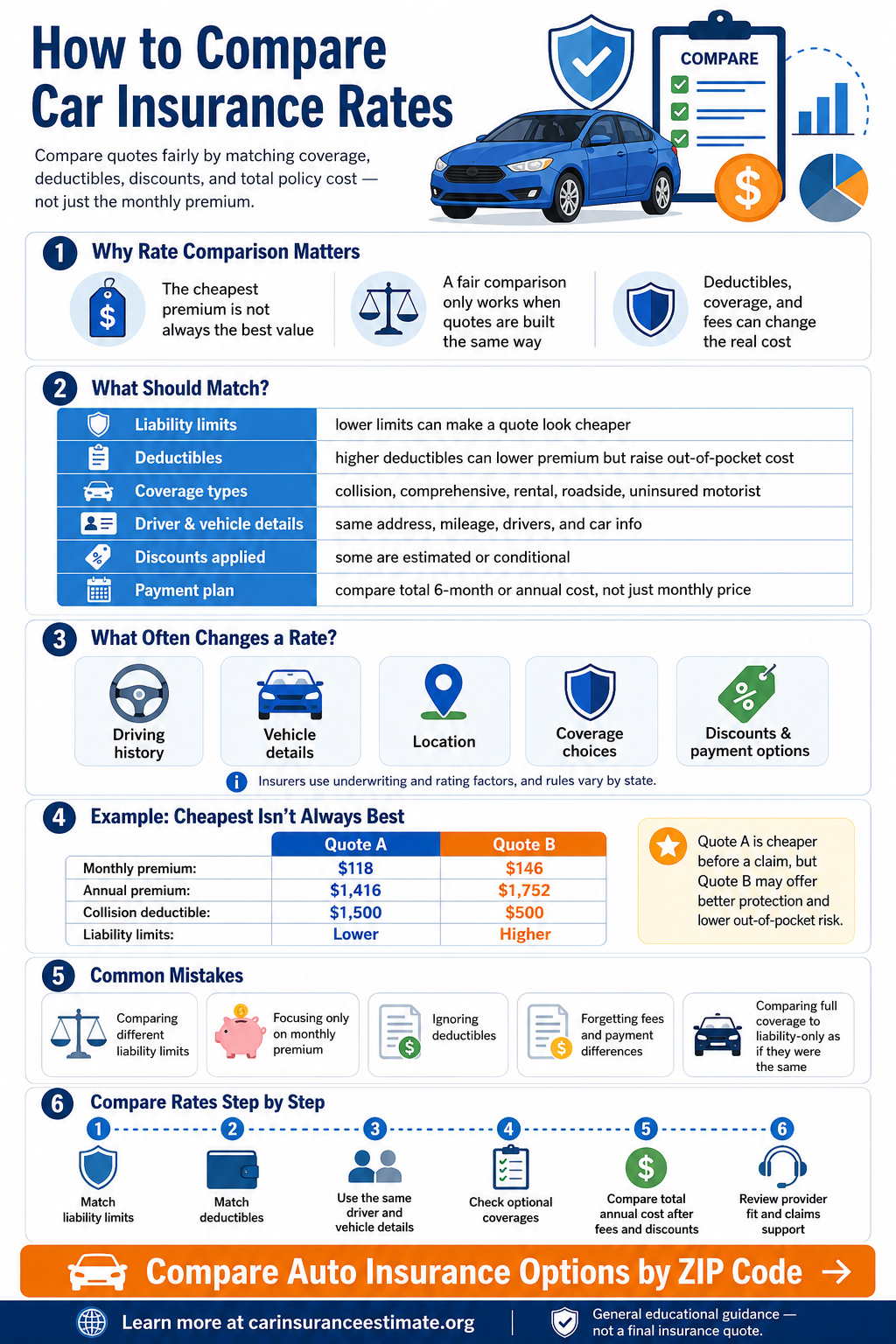

Why Rate Comparison Matters

A rate comparison page is useful because it helps drivers slow down and compare policies on more than price alone. A lower premium can come from weaker limits, fewer protections, a higher deductible, or discounts that may not apply after underwriting. A slightly higher premium can sometimes give better value if the policy structure is stronger.

The National Association of Insurance Commissioners explains that what you pay for auto insurance is generally shaped by two major processes: underwriting and rating. Underwriting helps the insurer evaluate the risk of the applicant, while rating assigns a price based on what the insurer believes it may cost to cover a potential claim. [1]

- A rate comparison is only fair when the quotes are built the same way. If Quote A has lower limits than Quote B, the lower price may simply reflect less protection.

- The cheapest premium is not always the best overall value. Deductibles, coverage gaps, and claim support can matter as much as the monthly payment.

- A stronger comparison helps you avoid choosing a weak policy by mistake. It forces you to review what the policy actually includes before you buy.

What Should Match When You Compare Rates?

The biggest mistake drivers make is comparing quotes that are not actually equivalent. If one quote has different liability limits, a different deductible, or more optional protections, the lower price may not mean much. Before comparing providers, make the policy settings as similar as possible.

| What to Match | Why It Matters | What to Check Before Choosing |

|---|---|---|

| Liability limits | A lower-priced policy may simply offer less protection for injury or property damage you cause to others. | Check bodily injury and property damage limits side by side. |

| Deductibles | A high deductible can reduce premium but increase your out-of-pocket cost after a covered claim. | Ask whether you could comfortably pay the deductible if an accident happened tomorrow. |

| Coverage types | Collision, comprehensive, uninsured motorist, roadside assistance, rental reimbursement, and other add-ons affect both price and value. | Confirm which coverages are included and which ones were removed to lower the price. |

| Driver and vehicle details | Different assumptions can produce very different rates, even with the same company. | Use the same garaging address, mileage, vehicle use, drivers, and vehicle information. |

| Discounts applied | Some quotes include discounts upfront while others require proof or eligibility checks. | Review whether discounts are guaranteed, conditional, or only estimated. |

| Payment plan | Monthly payments may include installment fees, while paid-in-full options may reduce total cost. | Compare total six-month or annual cost, not only the monthly bill. |

What Often Changes a Car Insurance Rate?

Even before you compare one insurer against another, your own quote can shift depending on the information provided. Quote results are usually starting points rather than final guarantees because insurers may verify driving records, vehicle details, claims history, prior insurance, garaging address, and eligibility for discounts.

NAIC lists common rating factors that may affect auto insurance prices, including location, age, gender, marital status, driving experience, driving record, claims history, credit history, previous insurance coverage, vehicle type, vehicle use, miles driven, chosen coverages, and deductibles. Rules vary by state, and not every factor is allowed or used the same way everywhere. [2]

- Driving history: accidents, claims, and violations can affect price because they may signal higher risk.

- Vehicle details: year, make, model, trim, repair costs, safety features, and theft risk can all influence the rate.

- Location: rates often vary by garaging address, traffic density, theft patterns, accident frequency, and state coverage rules.

- Coverage choices: stronger liability limits, lower deductibles, collision, comprehensive, and added protections usually change the premium.

- Discounts and payment options: bundling, safe-driver programs, paid-in-full discounts, paperless billing, or automatic payments can change the final result.

If you want to go deeper into quote factors, you can also explore Estimate Car Insurance Calculator, Auto Insurance Calculator, and Car Insurance Estimator.

Example: Why the Cheapest Monthly Rate Can Be Misleading

Imagine two quotes for the same driver and vehicle. Quote A costs $118 per month and Quote B costs $146 per month. At first glance, Quote A looks better because it saves $28 per month. Over a year, that is $336 in premium savings.

But now look at the deductible and coverage details. Quote A has a $1,500 collision deductible and state-minimum liability limits. Quote B has a $500 collision deductible and higher liability limits. If the driver has one covered collision claim, Quote A may require $1,000 more out of pocket before coverage responds. The monthly savings may not be enough to justify that extra risk for a driver with limited emergency savings.

| Comparison Item | Quote A | Quote B | Why It Matters |

|---|---|---|---|

| Monthly premium | $118 | $146 | Quote A is cheaper before a claim. |

| Annual premium | $1,416 | $1,752 | Quote A saves $336 per year before fees or claims. |

| Collision deductible | $1,500 | $500 | Quote B may be easier to handle after a covered accident. |

| Liability limits | Lower | Higher | Quote B may offer more financial protection after a serious accident. |

The better quote is not always the one with the lowest monthly number. The better quote is the one that matches your budget, vehicle, coverage needs, and ability to handle a deductible.

How Deductibles Affect Rate Comparison

Deductibles are one of the easiest ways to change the price of collision and comprehensive coverage. A higher deductible usually lowers the premium because you agree to pay more out of pocket before the coverage responds. That can be a smart choice for some drivers, but it becomes risky when the deductible is higher than your emergency savings.

The Insurance Information Institute notes that choosing higher deductibles can lower auto insurance costs, but also warns that drivers should make sure they have enough money set aside to pay the deductible if they have a claim. That point is important because a policy is not truly affordable if the monthly premium is low but the deductible would be difficult to pay. [3]

How Discounts Can Distort a Rate Comparison

Discounts can make a quote look attractive, but they should be reviewed carefully. Some discounts are easy to understand, such as multi-policy, multi-car, safe-driver, paperless billing, or paid-in-full savings. Others may depend on telematics participation, usage-based driving data, continuous coverage, or eligibility that must be verified.

A quote with many discounts is not automatically better than a quote with fewer discounts. What matters is the final premium, the coverage included, and whether those discounts will still apply when the policy renews. For that reason, compare the final policy cost after discounts, then review the coverage structure again.

Common Mistakes During Rate Comparison

Rate comparison works best when it is done with patience. Many bad decisions happen because the driver sees one low number and stops reviewing the rest of the policy.

- Comparing quotes with different liability limits.

- Ignoring deductibles while focusing only on the monthly premium.

- Assuming one insurer is always cheapest for every driver type.

- Choosing a quote before checking optional protections and exclusions.

- Comparing one quote with full coverage against another quote with liability-only coverage.

- Forgetting to include policy fees, installment fees, or payment-plan differences.

- Not checking whether the quote includes every household driver who must be listed.

- Stopping at price without reviewing provider fit or policy structure.

When the Cheapest Rate Is Not the Best Choice

A lower premium can still be the wrong choice if it leaves you underinsured or creates an out-of-pocket risk you cannot comfortably handle. This is especially important when comparing policies for newer vehicles, financed vehicles, leased vehicles, or households that need broader protection.

A cheap policy can make sense when the driver understands the trade-off. For example, liability-only coverage may be reasonable for an older vehicle with low market value. A higher deductible may be reasonable for a driver with strong savings. But those choices should be intentional, not hidden inside a quote that simply looks cheaper.

That is why it helps to compare this page with Cheap Full Coverage Car Insurance, Provider Reviews, Compare Providers, and Best Auto Insurance Comparison Sites.

How to Compare Car Insurance Rates Step by Step

| Step | What to Do | Why It Helps |

|---|---|---|

| 1 | Choose the same liability limits for every quote. | This prevents a low-limit policy from looking cheaper than a stronger policy. |

| 2 | Use the same deductibles for collision and comprehensive coverage. | This makes the premium comparison more accurate. |

| 3 | Enter the same vehicle, mileage, garaging address, and driver details. | Small differences in inputs can create different prices. |

| 4 | Check whether optional coverages are included or removed. | Roadside assistance, rental reimbursement, and uninsured motorist coverage can affect value. |

| 5 | Compare total six-month or annual cost after discounts and fees. | The monthly payment may not show the full cost of the policy. |

| 6 | Review the provider, claims process, and service style. | A slightly higher premium may be worth it if the policy is easier to manage and use. |

Frequently Asked Questions

What is the most important rule when comparing rates?

Make sure the quotes are based on similar limits, deductibles, coverage selections, driver details, and vehicle information. Without that, the comparison is weak.

Why can one insurer be much cheaper than another?

Different insurers weigh risk factors differently. One company may price your profile more favorably, while another may see the same driver, vehicle, or location as higher risk.

Should I always choose the lowest premium?

Not automatically. A lower price is only better when the policy still gives you the protection, deductible level, and provider fit that make sense for your situation.

How many car insurance quotes should I compare?

Comparing at least three quotes is a practical starting point because prices can vary significantly by insurer, driver profile, state, vehicle, and coverage selection.

Can changing my deductible lower my rate?

Yes, a higher deductible can lower the premium for some coverages, but only choose a deductible you could realistically pay after a covered claim.

Do credit-based insurance scores affect car insurance rates?

In states where allowed, some insurers may use credit-based insurance information as part of underwriting or rating. State rules vary, so this factor does not apply the same way everywhere.

Final Thoughts

Comparing car insurance rates works best when you look beyond the lowest premium and review what each policy actually includes. A quote can only be judged fairly when the coverage limits, deductibles, optional protections, discounts, fees, and driver details are similar.

A careful rate comparison can help you find a policy that balances affordability and protection more effectively. Before making a final decision, take time to review the coverage details, check which discounts are included, and confirm that the quote still fits your real needs.