Analyze the Real Cost Behind a Car Insurance Quote

A car insurance quote can look affordable at first glance, but the monthly premium is only one part of the decision. A stronger cost review looks at the premium, deductible, coverage level, policy fees, discounts, and the amount you may need to pay out of pocket after a claim.

This cost analyzer helps you compare the financial trade-offs behind two quote options before you move forward. It does not replace a final quote from an insurer, but it can help you understand whether a policy is truly affordable or only looks cheap on the surface.

Monthly Premium

The premium shows what you pay to keep the policy active, but it does not show the full financial exposure behind the policy.

Deductible Risk

A higher deductible may lower the monthly price, but it can increase what you would need to pay after a covered loss.

Total Policy Fit

The better question is whether the policy balances cost, coverage, deductible comfort, and real-world protection.

Simple Car Insurance Cost Analyzer

Enter two quote options to compare the estimated policy-term cost and the possible cost after one deductible event. This is a planning tool only. Final premiums, fees, and claim payments depend on the insurer and policy terms.

Quote A

Quote B

This tool uses simple math: monthly premium multiplied by 12, plus estimated fees, plus deductible when comparing a possible out-of-pocket event. It does not predict claims, underwriting decisions, coverage approval, or final insurer pricing.

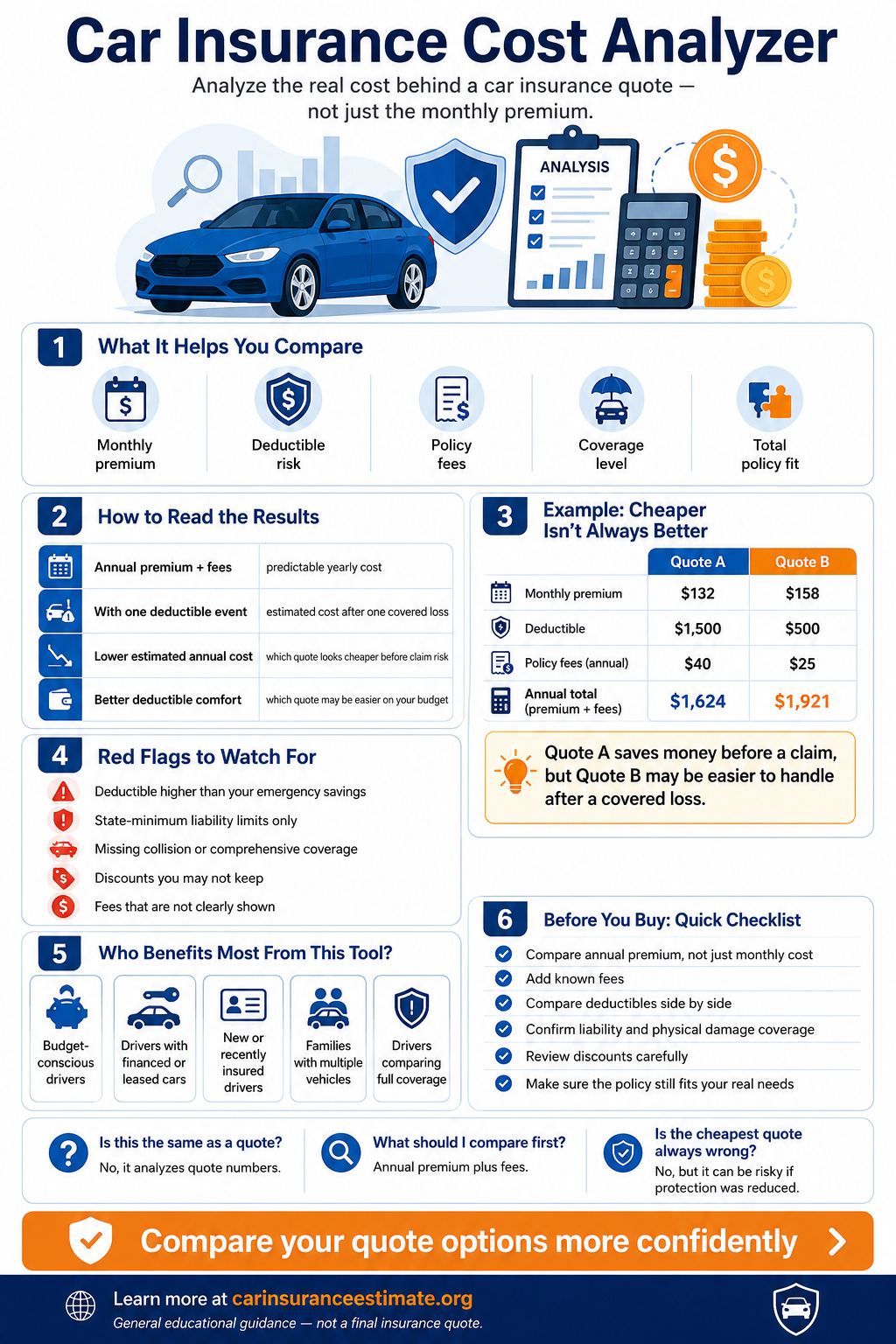

How to Read the Results From the Cost Analyzer

The cost analyzer is not meant to tell you which insurance company is best. Its purpose is to show how the numbers behind two quotes can change once you include the annual premium, estimated fees, and deductible exposure. This is important because the lower monthly payment is not always the lower-risk choice.

For example, Quote A may cost $145 per month with a $1,000 deductible, while Quote B may cost $170 per month with a $500 deductible. At first, Quote A looks cheaper because the monthly payment is lower. Over a full year, however, the difference may become less obvious once you add fees and think about what would happen after one covered claim.

This is why the analyzer separates annual premium cost from deductible risk. The annual premium shows the predictable cost of keeping the policy active. The deductible event estimate shows what the policy may feel like if you actually need to use collision or comprehensive coverage. Both numbers matter, but they answer different questions.

| Result Shown | What It Helps You Understand | How to Use It |

|---|---|---|

| Annual premium + fees | The estimated predictable yearly cost before any claim happens. | Use this to compare the basic cost of keeping each policy active. |

| With one deductible event | The estimated cost if you pay the annual premium, fees, and one deductible. | Use this to judge whether the lower premium is still worth it after a possible covered loss. |

| Lower estimated annual cost | Which quote appears cheaper before considering claim risk. | Do not choose based on this alone unless coverage and deductibles are also similar. |

| Better deductible comfort | Which quote may be easier to handle after a covered claim. | Use this if your emergency savings are limited or you want less out-of-pocket risk. |

Example: When the Lower Monthly Premium Is Not the Better Deal

Imagine two drivers comparing similar policies. Quote A is $132 per month with a $1,500 deductible and $40 in estimated fees. Quote B is $158 per month with a $500 deductible and $25 in estimated fees. Quote A looks cheaper because the monthly payment is $26 lower. Over twelve months, Quote A would cost about $1,624 before a claim, while Quote B would cost about $1,921 before a claim.

Before a claim, Quote A saves about $297 for the year. But if the driver has one covered accident where the deductible applies, Quote A could require $1,000 more out of pocket than Quote B. In that situation, the lower premium may not feel like a better deal. The right answer depends on the driver’s savings, vehicle value, risk tolerance, and whether the deductible is realistic.

This does not mean the higher-premium quote is always better. It simply means the decision should be based on more than the monthly payment. A driver with strong savings and a lower-value car may accept a higher deductible. A driver with a financed vehicle, tight monthly budget, or limited emergency fund may prefer a lower deductible even if the monthly premium is higher.

Why a Cost Analyzer Is Different From a Quote Calculator

A car insurance calculator usually helps you estimate a possible price range before you request a more specific quote. A cost analyzer works later in the shopping process. It helps you review the quote you already have and decide whether the price still makes sense after you include deductible risk, coverage quality, and possible fees.

That difference matters because two quotes can look close on the monthly payment but feel very different when you compare the deductible, coverage limits, and out-of-pocket exposure. If you are still at the estimate stage, start with the car insurance calculator. If you already have numbers to compare, this cost analyzer can help you review them more carefully.

What to Include When You Analyze Car Insurance Cost

The monthly premium is the easiest number to notice, but it should not be the only number you compare. A stronger review looks at the full policy structure, including deductibles, liability limits, optional coverages, fees, discounts, and the way each quote would work if a claim happens.

| Cost Factor | What It Means | Why It Can Change the Real Value |

|---|---|---|

| Monthly premium | The recurring cost to keep the policy active. | A lower premium may be helpful, but it can also reflect weaker limits, fewer protections, or a higher deductible. |

| Deductible | The amount you may need to pay before certain coverages respond to a claim. | A higher deductible can reduce the premium but increase your out-of-pocket burden after a covered loss. |

| Liability limits | The maximum amount the policy may pay for covered injury or property damage you cause to others. | Lower limits can make a policy cheaper, but they may also leave less protection after a serious accident. |

| Collision and comprehensive | Optional physical damage coverages that may help protect your own vehicle depending on the loss. | Removing them may lower cost, but it can be a poor fit for financed, leased, newer, or higher-value vehicles. |

| Discounts | Potential price reductions based on driver, vehicle, payment, policy, or household factors. | A discount only matters if the final policy still gives the coverage and deductible setup you actually want. |

| Policy fees | Possible installment, processing, policy, or service fees depending on the provider. | Fees can make one quote less attractive even when the base monthly premium looks lower. |

How to Compare Two Quotes Without Getting Misled

The most common mistake is comparing two quotes that are not built the same way. One policy may look cheaper because it has lower liability limits, a higher deductible, or missing protections. Another may look more expensive because it includes broader coverage or a lower deductible.

Before deciding that one quote is better, compare the structure first. If the limits, deductibles, and included coverages are not similar, the price comparison is weak. For a deeper side-by-side shopping process, use the rate comparison guide after reviewing your numbers here.

A quote is only “cheaper” in a useful way when the coverage behind it still fits your vehicle, budget, lender requirements, and risk comfort.

Cost Analyzer Red Flags to Watch For

A quote deserves closer review when the price looks unusually low compared with other options. Sometimes the quote is genuinely competitive. Other times, the low price comes from weaker coverage, missing protections, or a deductible that would be hard to pay after an accident.

- The deductible is much higher than your emergency savings. A high deductible can lower the premium, but it can create stress if you cannot pay it after a covered loss.

- The liability limits are only the state minimum. Minimum coverage may satisfy legal requirements, but it may not provide enough financial protection after a serious accident.

- Collision or comprehensive coverage is missing. This can reduce the premium, but it may not work for financed, leased, newer, or higher-value vehicles.

- The quote includes discounts you may not keep. Some savings depend on payment method, telematics participation, bundling, safe driving, or continuous coverage.

- Fees are not clearly shown. Installment fees, policy fees, or processing fees can make a quote more expensive than it first appears.

Premium vs. Deductible: The Trade-Off to Watch

A deductible can change how affordable a policy feels. Choosing a higher deductible may reduce the premium, but it can also create a larger bill if a covered claim happens. Choosing a lower deductible may raise the premium, but it can make the policy easier to manage after a loss.

There is no single right deductible for every driver. The better question is whether the deductible is realistic for your emergency budget. If the premium savings are small but the deductible becomes difficult to pay, the cheaper quote may not be as strong as it first appears.

If you are mainly focused on low prices, also read the guide on the risks of choosing the cheapest car insurance before selecting a policy only because the monthly number is lower.

Which Drivers Benefit Most From a Cost Analyzer?

This type of tool is most useful for drivers who already have at least two quote options and want to compare the real trade-offs. It is especially helpful when one quote has a lower premium but a higher deductible, or when one policy includes stronger coverage that makes the monthly cost look higher.

| Driver Situation | Why the Analyzer Helps | What to Focus On |

|---|---|---|

| Budget-conscious driver | Shows whether a cheap monthly premium still creates manageable out-of-pocket risk. | Annual cost, fees, and deductible comfort. |

| Driver with a financed or leased car | Helps compare broader coverage options that may be required by a lender or lessor. | Collision, comprehensive, deductible, and full policy cost. |

| New driver or recently insured driver | Makes it easier to understand why quotes vary and where the cost is coming from. | Coverage limits, deductible, prior insurance history, and discounts. |

| Family with multiple vehicles | Helps compare total cost when small monthly differences multiply across several cars. | Bundling, multi-car discounts, fees, and annual total. |

| Driver comparing full coverage | Shows how deductible choices affect the real cost of broader protection. | Premium, deductible, vehicle value, and claim affordability. |

When a Lower-Cost Policy Can Still Make Sense

A lower-cost policy is not automatically a bad decision. It can make sense when the coverage level is intentional, the deductible is manageable, and the vehicle situation does not require broader protection. The problem is choosing a lower price without understanding what changed inside the quote.

- The deductible is affordable if you need to file a covered claim.

- The liability limits still feel reasonable for your risk level.

- The policy includes the coverages you actually meant to buy.

- The quote is being compared against similar policy structures.

- Any discounts or fees are clearly reflected in the final cost.

How Coverage Type Changes the Cost Picture

The cost analyzer becomes more useful when you know what kind of policy you are reviewing. Liability-only, minimum coverage, and broader full coverage policies should not be judged as if they are the same product.

If you are still unsure what liability, collision, comprehensive, uninsured motorist coverage, or optional protections mean, review the type of coverage guide before relying too heavily on price. If you are specifically comparing broader protection, continue to cheap full coverage car insurance after using this analyzer.

Discounts Should Be Reviewed After the Policy Structure

Discounts can help lower the final price, but they should not replace a coverage review. A discounted policy can still be a weak fit if the deductible is uncomfortable, the limits are too low, or the coverage leaves out protections you expected.

Use discounts as the second layer of the decision. First check whether the policy itself makes sense. Then review whether the available savings improve the value. For more detail, visit discounts and offers.

Cost Analyzer Checklist Before You Buy

- Write down the monthly premium for each quote.

- Multiply the monthly premium by 12 to estimate annual premium cost.

- Add known policy, installment, or processing fees if they apply.

- Compare deductibles side by side, not separately from the premium.

- Confirm liability limits, collision, comprehensive, and optional protections.

- Check whether discounts are guaranteed or only possible.

- Review whether the lowest-cost option still fits your real needs.

Frequently Asked Questions

Is a car insurance cost analyzer the same as a quote?

No. A cost analyzer helps you compare the numbers behind a quote. It does not create a final policy price, approve coverage, or replace the insurer’s underwriting process.

What number should I compare first?

Start with the annual premium plus known fees because that shows the predictable yearly cost. Then compare deductible exposure because that shows what the quote may feel like if you actually need to use the policy. Finally, compare coverage structure. Looking only at the monthly payment can make a weaker policy look stronger than it really is.

Is the cheapest quote always the wrong choice?

Not always. A cheaper quote can be a good fit if the coverage, deductible, and provider still match your needs. It becomes risky when the lower price comes from protection you did not mean to remove, a deductible you cannot comfortably pay, or fees that were not obvious when you first compared the monthly premium.

Should I use this before or after instant quotes?

Use this after you have quote numbers to compare. If you have not started yet, begin with instant quotes and then return here to analyze the cost trade-offs.

Does a higher deductible always save enough money?

No. A higher deductible may lower the premium, but the savings should be compared with what you would need to pay after a covered loss. The deductible should still fit your real budget.

Can this analyzer help me choose between full coverage and liability-only insurance?

It can help you compare cost trade-offs, but it does not decide which coverage type is right for you. Full coverage usually costs more because it can include collision and comprehensive protection for your own vehicle. Liability-only coverage may be cheaper, but it generally does not pay to repair or replace your own car after many types of losses.

Why do two quotes with similar monthly prices feel so different?

Two quotes can have similar premiums but very different deductibles, limits, fees, exclusions, or optional coverages. That is why it is important to compare the full policy structure instead of only comparing the monthly payment.

References

Ready to Compare Quote Options?

After reviewing the real cost behind your policy options, enter your ZIP code to continue comparing available auto insurance paths.