How to Compare Car Insurance Providers the Smart Way

Comparing car insurance providers is not just about finding the lowest monthly payment. A good comparison looks at the full policy: liability limits, deductibles, collision and comprehensive coverage, uninsured motorist protection, discounts, payment options, claims support, and whether the company fits the way you prefer to manage insurance.

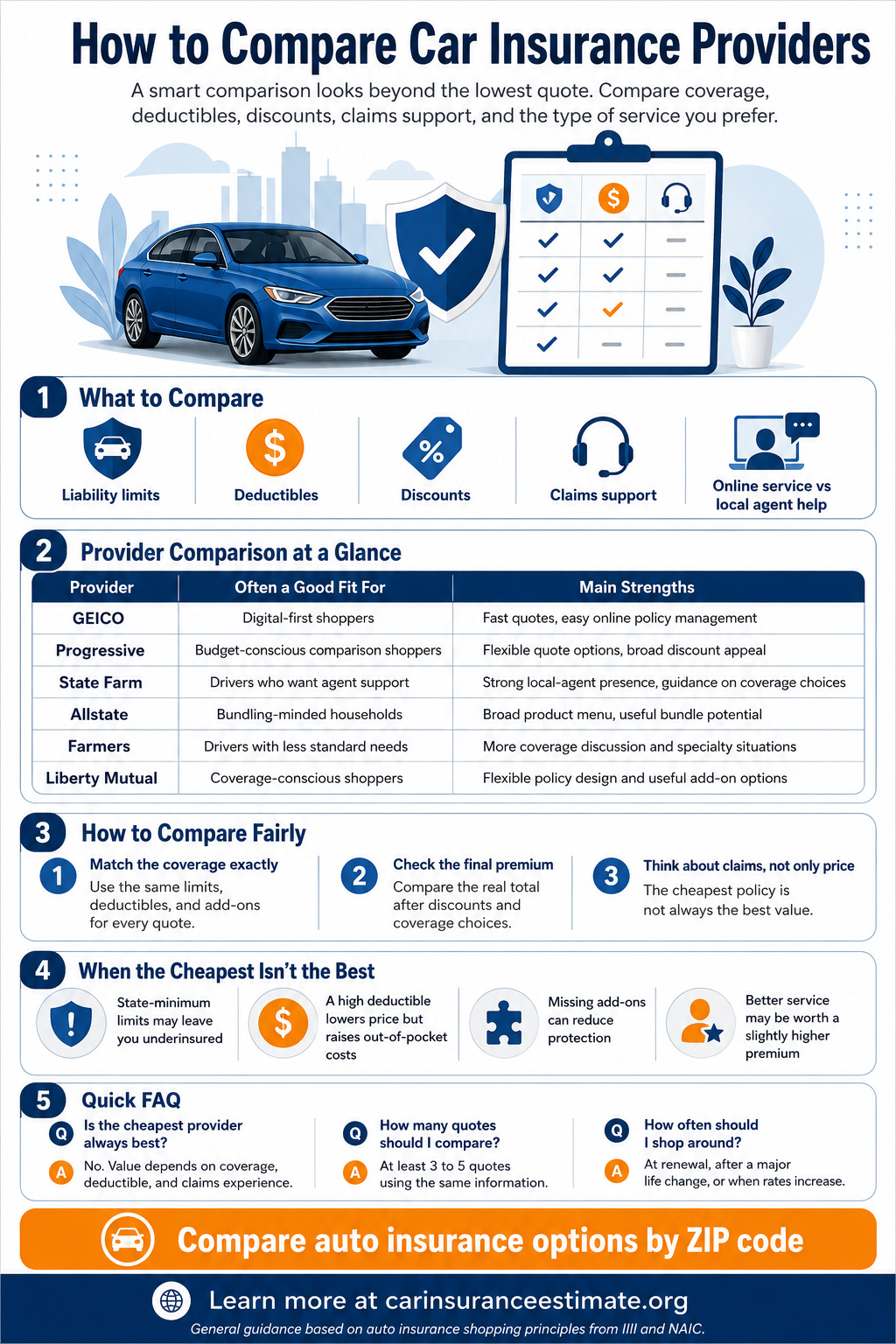

The Insurance Information Institute recommends comparing policies from at least three insurers and making sure the policies have the same types and amounts of coverage. That matters because a quote with lower limits or a higher deductible may look cheaper, even though it gives you less protection. If you want a broader starting point before narrowing down carriers, explore our provider reviews and this guide to best auto insurance comparison sites. [1]

Best for digital-first shoppers

Some insurers are easier to manage online, with fast quotes, cleaner apps, and simpler policy changes.

Best for agent support

If you want help choosing limits, bundling policies, or handling a claim, an insurer with a strong agent network can feel more reassuring.

Best for customization

Drivers with unusual needs often do better with carriers that offer more deductible, endorsement, and coverage combinations.

Best for value, not just price

The cheapest quote can still be expensive if it leaves you underinsured, makes claims harder, or removes useful protections.

Provider Comparison at a Glance

These provider notes are general shopping guidance, not a guarantee that one company will be cheapest for your profile. Auto insurance prices vary by state, ZIP code, age, vehicle, driving record, prior insurance, selected coverage, and underwriting rules. NAIC explains that insurers use underwriting to evaluate risk and rating to assign a price based on the insurer’s expected cost of covering a potential claim. [2]

| Provider | Often a Good Fit For | Main Strengths | Potential Drawbacks |

|---|---|---|---|

| GEICO | Drivers who want a simple online experience and competitive everyday pricing. | Strong quote flow, easy policy management, and good appeal for self-service shoppers. | May feel less personal if you prefer agent-led advice and in-person support. |

| Progressive | Drivers who like comparing options and adjusting coverage to fit a target budget. | Flexible shopping experience, broad discount appeal, and useful quote comparison tools. | Some profiles may still see higher pricing once accidents, violations, or stronger coverage are included. |

| State Farm | People who want agent support and a more traditional insurance relationship. | Strong local-agent presence, useful for bundling and discussing coverage choices. | Not always the lowest-priced option for shoppers focused only on rate. |

| Allstate | Households comparing multiple policy types and looking at safe-driving incentives. | Broad product menu, solid bundling potential, and useful options for drivers who want more than basic auto coverage. | Can be priced above leaner competitors for some shoppers. |

| Farmers | Drivers who value coverage conversations and specialty situations more than bare-minimum simplicity. | Good fit when you want more guidance or need less standard policy options. | Online experience may feel less streamlined than the most digital-first brands. |

| Liberty Mutual | Drivers who want more control over how a policy is structured. | Flexible coverage design and useful add-on options for shoppers who care about tailoring protections. | Base pricing can feel high before discounts, depending on profile and state. |

What Actually Makes One Provider Better Than Another?

The best provider is the one that gives you the right coverage at a price you can afford, with service you trust if you ever need to file a claim. That means two drivers in the same city can make completely different choices and both be right. One may need the cheapest legal coverage for an older car. Another may need full coverage, rental reimbursement, roadside assistance, and higher liability limits because they drive daily with family passengers.

| Comparison Factor | Why It Matters | Question to Ask Before Buying |

|---|---|---|

| Liability limits | Higher limits can protect you better after an at-fault accident, but they usually cost more. | Are the limits high enough for my assets, income, and driving risk? |

| Deductible | A higher deductible can lower premium, but it also means you pay more out of pocket after a claim. | Could I comfortably pay this deductible tomorrow if something happened? |

| Claims support | The cheapest policy may not feel cheap if the claims process is stressful or slow. | Does this insurer make it easy to report, track, and resolve claims? |

| Discounts | Discounts can help, but the final premium matters more than the number of discounts advertised. | What is the final price after discounts, fees, and coverage changes? |

| Local vs online service | Some drivers want a local agent, while others prefer apps, online documents, and fast self-service. | How do I actually want to manage this policy after I buy it? |

Detailed Provider Notes

Strong for fast quotes and straightforward shopping

GEICO often appeals to drivers who want to get a quote quickly, manage a policy online, and avoid a lot of back-and-forth. It can be a practical option for drivers who already know the coverage they want and prefer a clean digital experience.

- Best for: online-first shoppers, routine policy management, and simple quote flow.

- Watch for: less appeal if you want regular help from a dedicated local agent.

- Good question to ask: is the quote still competitive after adding the limits and deductibles you actually want?

Good for shoppers who want options and quote flexibility

Progressive is often attractive to people who like comparing several coverage combinations before choosing. It can work well for drivers who want to fine-tune a policy rather than accept the first quote shown.

- Best for: budget-conscious comparison shoppers and drivers testing multiple coverage levels.

- Watch for: pricing can change meaningfully when risk factors or stronger protections are added.

- Good question to ask: how much of the quote depends on reducing useful coverage?

Often strongest when personal guidance matters

State Farm tends to make the most sense for shoppers who want to talk through liability limits, deductibles, bundling, or claim scenarios with a real person rather than handling everything through a screen.

- Best for: local support, families, and drivers who want help choosing coverage.

- Watch for: not always the lowest quote if you are focused only on price.

- Good question to ask: what extra value do you get from agent support compared with the price difference?

Worth a look for broader household insurance planning

Allstate often gets attention from shoppers comparing auto together with home, renters, or other policy types. It can make sense when the goal is to simplify several policies under one company.

- Best for: bundling-minded households and drivers reviewing multiple products together.

- Watch for: a higher premium can erase the benefit if the bundle is not strong enough.

- Good question to ask: is the bundle discount real once all line items are compared side by side?

Useful when your situation is less standard

Farmers can be a better fit for people who want more conversation around coverage and who may have needs that do not fit a very stripped-down online quoting path.

- Best for: drivers who value stability, explanation, and a broader discussion of policy choices.

- Watch for: the buying experience may feel less frictionless than the most app-driven competitors.

- Good question to ask: are you paying more for service you will actually use?

Appealing for shoppers who want more policy tailoring

Liberty Mutual is often considered by drivers who care about shaping a policy around their exact needs rather than picking the simplest preset option.

- Best for: customization, add-on review, and coverage-conscious shoppers.

- Watch for: pricing may feel high before discounts are fully applied.

- Good question to ask: which add-ons are genuinely useful, and which ones only make the quote look fuller?

How to Compare Providers Before You Buy

A fair comparison should make every quote compete under the same conditions. NAIC’s auto insurance shopping materials point shoppers toward reviewing coverage limits, deductibles, uninsured and underinsured motorist coverage, discounts, and questions about how driving record or credit history can affect premiums. [3]

Match the coverage exactly

Use the same bodily injury limits, property damage limits, deductible, rental reimbursement, roadside help, and uninsured motorist settings for every quote.

Check discounts after the base quote

A strong advertised discount does not always mean the total premium ends up lower. Compare the final number, not just the promotion.

Think about claims, not only price

If you are ready to move from research to shopping, compare several instant quotes using the same information so you can judge real value rather than headline pricing.

When the Cheapest Provider May Not Be the Best

A low premium is attractive, but it should not be the only reason you choose a provider. For example, a policy can be cheaper because it has state-minimum liability limits, excludes useful optional coverages, uses a very high deductible, or does not include rental reimbursement. That might be fine for a driver who only needs basic legal coverage, but it may be risky for someone with a newer vehicle, a loan, a lease, or a longer daily commute.

The better question is not “Which company is cheapest?” but “Which company gives me the best value for the coverage I actually need?” If two quotes are close in price, the better company may be the one with easier claims tools, clearer policy documents, stronger customer support, or a discount structure that still works after renewal.

Frequently Asked Questions

Is the cheapest provider always the best choice?

No. A cheaper policy can become expensive if it cuts useful coverage, raises your deductible beyond what you can comfortably pay, or gives you a weaker claims experience.

Should I choose an online-first insurer or a local-agent insurer?

That depends on how you shop. If you like speed and self-service, digital-first carriers may feel easier. If you want help understanding limits, bundling, and claims scenarios, agent support can be worth paying a bit more for.

Why do quotes differ so much between providers?

Every insurer weighs risk differently. Your age, ZIP code, driving history, vehicle, annual mileage, prior insurance, and selected limits can shift one carrier from “cheap” to “expensive” very quickly.

What is the best way to compare providers fairly?

Run at least three to five quotes using the exact same information, then compare total premium, coverage details, deductible, discounts, and the overall fit for how you want to manage your policy.

How often should I compare car insurance providers?

It is smart to compare when your policy renews, when you move, when you add or remove a vehicle, after a major life change, or when your premium increases without a clear reason.

Bottom Line

There is no single best provider for everyone. The strongest choice is the one that balances price, usable coverage, claims confidence, and the kind of service you actually want. For readers who want to keep researching before buying, our provider reviews, rate comparison, and type of coverage resources are the best next stops.

- Compare identical coverage first.

- Look past the headline price.

- Choose the provider that matches your driving profile and support preference.

- Review the final premium, deductible, exclusions, and policy details before buying.