Car Insurance FAQ

Car Insurance FAQs: Estimates, Quotes, Coverage, and Provider Comparison

This FAQ page answers common questions about car insurance estimates, quote tools, coverage choices, provider comparison, and price differences. It is designed as a practical support page for shoppers who want clearer next steps before choosing a policy.

Car insurance prices can change based on driver information, vehicle details, location, coverage limits, deductibles, discounts, and insurer underwriting rules. That is why a useful FAQ should do more than send readers to another page. It should explain what the terms mean, why quotes can change, and how to compare options more fairly.

If you want to go deeper while you compare, you can also visit Instant Quotes, Type of Coverage, Rate Comparison, Compare Providers, Car Insurance Guide, and Resources.

Estimate vs. quote

Understand why an estimate is a planning tool, while a final quote can change after full underwriting and review.

Coverage choices

See how deductibles, liability limits, and full coverage decisions can affect both price and policy value.

Better comparison

Learn how to compare companies more fairly by matching policy structure instead of looking only at the lowest number.

Best Next Page to Visit by Topic

Frequently Asked Questions

1. What is the difference between a car insurance estimate and a car insurance quote?

A car insurance estimate is usually an early price range based on limited information. It helps you understand what your policy might cost before you complete a full application. A quote is typically more detailed because it reflects more specific rating information, policy choices, and review steps.

That distinction matters because shoppers sometimes compare one company’s estimate against another company’s more complete quote and assume the lower number is automatically better. The better approach is to keep the structure as consistent as possible across every option you review. You can continue that comparison on Insurance Estimates, Instant Quotes, and Car Insurance Estimator.

2. How accurate is an online car insurance estimate?

An online estimate can be useful for planning, but it is still a starting point rather than a final guarantee. The closer your information matches the policy details a carrier reviews later, the more useful the estimate tends to be. Even then, the final price may still change once the insurer confirms rating details and the exact coverage structure.

That is why it helps to treat estimates as a comparison tool instead of a promise. They are most useful when you want to narrow down options, compare rough pricing paths, and decide which companies deserve a closer look. For a more structured comparison, visit Rate Comparison and How Car Insurance Estimates Work.

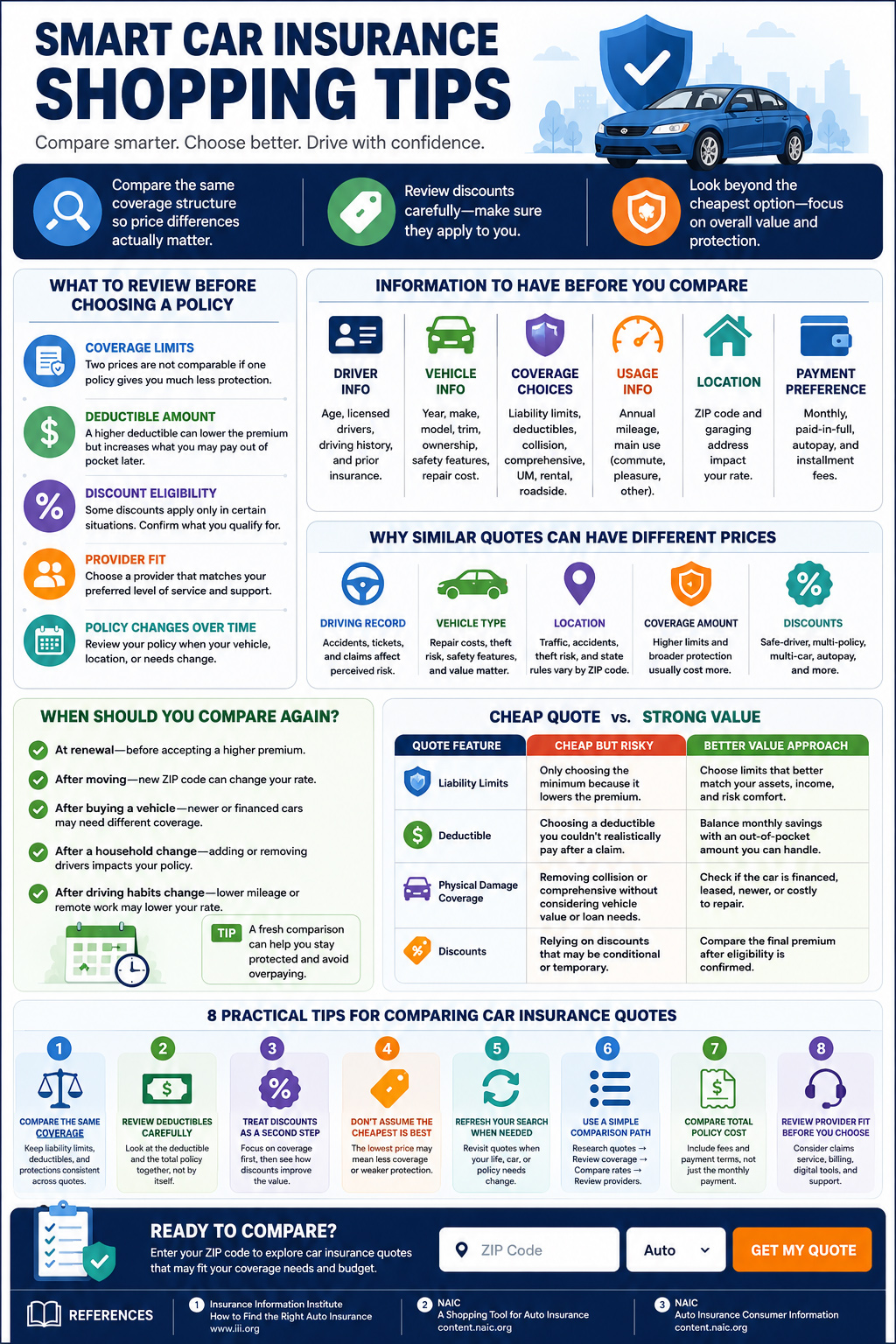

3. What information do I usually need to get a car insurance estimate?

Most estimate tools work best when you enter consistent basics such as your ZIP code, vehicle details, driver profile, desired coverage level, and deductible preferences. Some tools may ask for more than others, but the main goal is always the same: to create a policy structure that is detailed enough to support a realistic comparison.

The more important point is consistency. If you change deductibles, liability limits, or coverage types from one company to another, the numbers stop being easy to compare fairly. That is why many shoppers benefit from reviewing Type of Coverage before they start comparing prices.

4. Do I need a Social Security number to compare options?

Not always at the earliest research stage. Some shoppers begin with general estimate tools or simplified quote paths before deciding whether to continue with a more complete application. The exact process depends on the insurer, the quote path, and how detailed the request becomes.

The practical takeaway is that you can often begin researching without treating the first step like a full commitment. If this is a major concern for your comparison process, the most relevant page on the site is Auto Insurance Quote Without SSN.

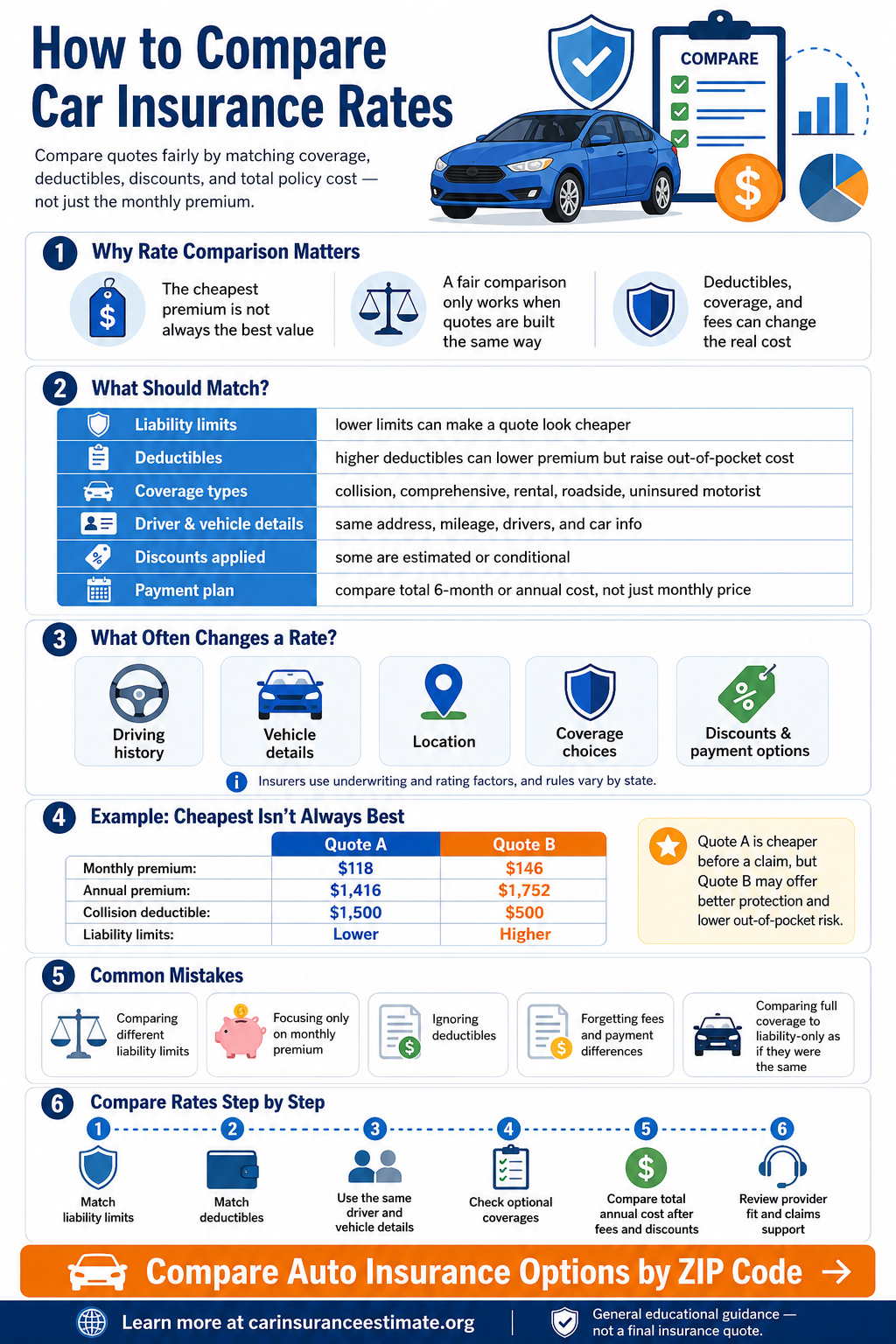

5. Why do coverage limits and deductibles change the price so much?

Price is never just about the company name. It is also about what the policy is built to do. Higher liability limits, lower deductibles, and broader protection can raise the premium because the policy is designed to provide more protection. On the other hand, a cheaper policy may simply reflect less coverage, a higher deductible, or fewer optional protections.

This is one of the biggest reasons shoppers get confused when they compare insurers. A low number only tells part of the story. The better question is whether the policy structure fits your needs. A good place to keep that research organized is Type of Coverage and Cheap Full Coverage Car Insurance.

6. Why can two companies show very different prices for similar drivers?

Different insurers may evaluate risk, discounts, driving profile details, vehicle characteristics, and coverage packaging in different ways. That is why one company may look strong for one shopper while another carrier may look better for someone with a different vehicle, location, coverage target, or driver profile.

The key lesson is that brand familiarity does not guarantee the best result, and a single quote does not tell you enough about the broader market. The smarter move is to compare several similarly structured options and then review support model, discounts, and overall fit. Pages like Compare Providers, Provider Reviews, and Best Auto Insurance Comparison Sites can help you do that more carefully.

7. Is the cheapest car insurance policy always the best option?

Not automatically. A lower premium can be attractive, but the best value depends on what the policy includes, how the deductibles are set, and whether the protection matches your needs. A policy that looks cheaper at first can feel less useful later if it leaves you with weaker protection than you expected.

That is why it helps to compare price and policy design together. Use low price as a signal to investigate further, not as the only decision factor. For additional support, review Discounts and Offers, Car Insurance Basic, and Car Insurance Guide.

8. How can I compare car insurance providers more fairly?

Start by choosing the coverage structure you actually want. Then keep the main elements aligned across every quote: liability limits, deductibles, vehicle information, and optional protections. Once the structure is consistent, it becomes much easier to compare companies on price, support style, convenience, and overall fit.

A fair comparison also means looking beyond marketing language. Some shoppers prefer a digital-first experience, while others value agent access, support channels, or more flexible policy customization. That is why provider comparison should look at both price and policy experience. The best supporting pages for that step are Compare Providers, Provider Reviews, and Rate Comparison.

9. Do young drivers always pay more for car insurance?

Young drivers often see higher prices than older drivers with longer driving histories, but that does not mean every policy will look the same or that every company will price the same way. Coverage choices, vehicle type, location, and discount eligibility can still affect the outcome in meaningful ways.

That is why younger shoppers benefit from broad comparison rather than guessing based on one company or one ad. If that topic is central to your search, visit Car Insurance Quotes for Young Drivers and then continue comparing through Instant Quotes.

10. Can I estimate full coverage separately from basic or liability-focused coverage?

Yes. In practice, many shoppers compare more than one coverage path so they can understand the tradeoff between lower monthly cost and broader protection. That comparison is especially useful when you are trying to decide whether paying more gives you enough additional value for your situation.

Instead of treating every estimate as the same type of policy, it helps to review basic, liability-focused, and fuller coverage paths separately. The most useful pages for that are Car Insurance Basic, Cheap Full Coverage Car Insurance, and Type of Coverage.

11. How often should I refresh my car insurance estimate?

It makes sense to refresh your estimate when important details change, such as your location, vehicle, driver profile, coverage goals, or comparison priorities. Even when nothing dramatic has changed, revisiting the estimate can still help if you are moving from early research into active quote shopping.

The goal is not to check constantly. The goal is to revisit the process when your policy needs, budget priorities, or shopping stage becomes different from before. A practical next step is to review Car Insurance Estimator Get Accurate Quotes Online, Insurance Estimates, and Tools.

12. What is the best way to use this site before choosing a policy?

The best approach is to move in order. Start with educational pages so you understand estimates, coverage types, and the difference between lower price and better value. Then use calculators and comparison pages to narrow your options. After that, review provider-focused content to compare policy fit more carefully.

A simple path could look like this: Car Insurance Guide → Type of Coverage → Estimate Car Insurance Calculator → Rate Comparison → Compare Providers.

13. What factors usually affect a car insurance price?

Car insurance prices are usually based on a mix of driver, vehicle, location, coverage, and policy factors. The exact formula varies by insurer and state, but common factors can include driving record, claims history, vehicle type, ZIP code, annual mileage, coverage limits, deductible choices, prior insurance history, and available discounts.

This is why two drivers with similar vehicles can receive very different prices. One driver may have a cleaner driving record, lower annual mileage, stronger prior insurance history, or a garaging address in an area with fewer claims. Another driver may pay more because the insurer sees higher risk based on the information used for rating.

14. Why should I compare the same coverage limits across quotes?

Comparing different coverage limits can make a quote look cheaper than it really is. For example, one policy may show a lower premium because it uses state-minimum liability limits, while another quote may include higher liability limits, uninsured motorist coverage, rental reimbursement, or lower deductibles.

A fair comparison should keep the main policy structure as similar as possible. Match liability limits, collision and comprehensive deductibles, optional coverages, vehicle information, driver information, and payment terms. Once the structure is similar, the price difference becomes more meaningful.

15. What is the difference between liability-only and full coverage?

Liability-only coverage generally focuses on injuries or property damage you cause to others, up to the limits of the policy. It usually does not pay to repair or replace your own vehicle after an at-fault accident. Full coverage is not one single official coverage type, but shoppers often use the term to describe a policy that includes liability plus collision and comprehensive coverage.

Collision coverage may help pay for damage to your own vehicle after a covered crash, while comprehensive coverage may help with non-collision losses such as theft, vandalism, fire, hail, or certain weather-related damage. If your vehicle is financed or leased, your lender or leasing company may require physical damage coverage.

16. Why can an estimate change after I submit more information?

An estimate can change because early quote tools often use limited information. Once an insurer reviews more complete details, the price may adjust. That can happen after verifying your driving record, claims history, vehicle identification number, garaging address, prior insurance, household drivers, coverage selections, and discount eligibility.

This does not always mean the original estimate was wrong. It means the first number was based on a smaller set of assumptions. The closer your original information is to the final policy details, the more useful the estimate will usually be.

17. What deductible should I choose?

The right deductible depends on your budget and risk comfort. A higher deductible can lower the premium, but it also means you may need to pay more out of pocket after a covered claim. A lower deductible may cost more each month, but it can make the policy easier to use after an accident or covered loss.

A practical rule is to choose a deductible you could realistically pay without creating financial stress. If the premium savings are small but the deductible becomes difficult to afford, the cheaper monthly quote may not be the better value.

18. How many car insurance quotes should I compare?

Comparing at least three quotes is a practical starting point. Prices can vary because insurers weigh risk factors differently, offer different discounts, and package coverage in different ways. One insurer may be competitive for a driver with a clean record, while another may be better for a driver with a different vehicle, location, or coverage need.

The key is to compare quotes with the same assumptions. Use the same liability limits, deductibles, drivers, vehicle details, mileage, and coverage selections. That makes the comparison more useful than simply collecting several unrelated prices.

19. When should I review or compare my car insurance again?

It is smart to review your car insurance at renewal, especially if the premium increases. You should also compare again after moving, buying a car, selling a car, adding or removing a driver, changing your commute, paying off a vehicle loan, or deciding that your current deductible or coverage limits no longer fit your budget.

A quote that made sense last year may not be the best fit today. Your vehicle value, household drivers, driving habits, and coverage goals can change over time.

20. What should I check before buying a policy?

Before buying, review the declarations page or quote summary carefully. Check liability limits, deductibles, covered vehicles, listed drivers, effective date, payment schedule, discounts, optional coverages, exclusions, and whether the policy includes collision, comprehensive, uninsured motorist, rental reimbursement, or roadside assistance if you expected those protections.

Also confirm that the ZIP code, garaging address, vehicle use, mileage estimate, and driver information are accurate. Incorrect information can cause price changes or coverage issues later.

Key Car Insurance Terms Explained

| Term |

Plain-English Meaning |

Why It Matters |

| Premium |

The amount you pay to keep the policy active. |

A low premium can be useful, but it should be compared with coverage limits and deductibles. |

| Deductible |

The amount you may pay before certain coverages respond to a claim. |

A higher deductible can lower the premium but increase out-of-pocket risk. |

| Liability limit |

The maximum amount the policy may pay for covered damage or injuries you cause to others. |

Lower limits may reduce price but can leave less financial protection. |

| Collision coverage |

Coverage that may help repair or replace your vehicle after a covered crash. |

Often important for financed, leased, newer, or higher-value vehicles. |

| Comprehensive coverage |

Coverage that may help with non-collision losses such as theft, vandalism, fire, hail, or certain weather damage. |

Can add protection beyond accident-related damage. |

| Underwriting |

The process insurers use to evaluate risk and decide eligibility or pricing. |

Final pricing can change after more complete information is reviewed. |

Keep Comparing With More Clarity

This FAQ page works best when it helps you move to the next useful step. Whether you want faster quote research, better provider comparison, or more guidance on coverage choices, the pages below can help you continue with a more structured approach.

Ready to Compare?

Explore Car Insurance Quotes With More Clarity

Enter your ZIP code to continue comparing car insurance options and review quote paths that may fit your coverage needs and budget.